Pai and Think-Tank Ally Are Wrong About Net Neutrality

The latest claims from FCC Commissioner Ajit Pai and the Progressive Policy Institute’s Hal Singer on Title II and investment are 100 percent wrong. Both men are either willfully misleading people or dangerously ignorant of the facts.

Below is our lengthy and detailed analysis, carrier by carrier, but here are the highlights and a few explanations at the outset:

- Almost all of the observed first-quarter/second-quarter declines are due to AT&T. AT&T’s decline is due to its finishing Project VIP and returning to “normal” capex levels. AT&T told investors to expect this temporary bump and decline as far back as 2012.

- Singer neglected to include in his alleged analysis the massive increases in network spending at several companies, such as Comcast. In fact, if you look at actual network spending by cable companies (i.e., not set-top-box spending), capital investments in cable broadband networks are up this year.

- Much of the small decline at companies other than AT&T is not from a decline in network capital expenditures, but in set-top box spending. For example, Charter and Cablevision made large purchases on customer premise equipment in 4Q 2014, so there was no need to replicate that kind of expense earlier this year. These decreases in set-top box spending are not only predictable, they’re wholly unrelated to Title II.

- Singer’s choice to look at 1Q and 2Q is curious. There’s no reason to expect a decline in 1Q, since the FCC’s order didn’t receive a vote until two-thirds of the way through the quarter. 2Q to 2Q comparisons between 2014 and 2015 show increases in capital investments. That is, the spending in the first full quarter after reclassification was higher than it was during the same quarter the prior year.

- It’s also curious that Commissioner Pai chose to cite wireless capex. AT&T’s wireless capex is down because it finished its “Project VIP.” But wireless capex was up at Verizon, Sprint and T-Mobile.

All of these individual facts aside, what we have here is a selective sampling of company spending — including not only spending that goes to newly classified Title II broadband services and networks, but also spending on longstanding Title II voice services, Title VI cable services and unregulated services — with Singer attributing 100 percent of any change in that spending to a single cause: the FCC’s reclassification of broadband access as a Title II telecommunication service.

Analytically, this is just silly. There are many other factors that impact short-term capital allocation, and not a single one of the companies Singer cites have said that Title II had an impact.

In fact, if you read the statements they made to investors, they explain what’s behind any changes in spending quite clearly — both before and after the FCC voted.

In his Aug. 25 piece, Singer suggested that broadband investment was down because of the FCC’s Title II reclassification decision. In cherry-picking numbers to make his case, he selectively cited capital spending figures by five large ISPs: AT&T, Verizon, Charter, Cablevision and CenturyLink.

He did not discuss in depth spending at Comcast or Time Warner Cable, the nation’s #1 and #3 largest providers of residential broadband (hint, perhaps this is because their spending was up by double-digit percentages).

Singer’s claims are wildly misleading, as the details below show. The top-level summary is this:

The declines in capital spending cited by Singer were all announced well ahead of the FCC’s reclassification order, and reflect completions of projects by certain of these companies. This is not Free Press’ analysis or opinion of the cause for any such declines; it’s based on what the CEOs and CFOs of these companies have repeatedly told investors in public forums.

What’s more, most of the declines are not even in spending for these company’s Title II services and networks now classified as such by the FCC: they come from reduced spending on equipment like cable-television set-top boxes.

Finally, Singer neglected to mention that actual network investment (and not spending on set-top boxes) at many of these ISPs has been higher following the FCC’s February 2015 reclassification, and is likewise higher for the ISPs he neglected to discuss in any detail.

Indeed, Comcast announced the largest, fastest deployment of gigabit fiber (touting 2 gigabit speeds) in the history of the world following the FCC’s reclassification, but no mention of Comcast’s broadband network investments made Singer’s list.

Nor did AT&T’s recent announcement about increasing its fiber-deployment plans. Nor did CenturyLink’s recent announcement about expanding its fiber footprint. Nor did Time Warner Cable’s announcement of the acceleration of its DOCSIS 3 deployments. Nor did Suddenlink’s recently unveiled fiber plans. Nor did the fiber-expansion plans of smaller ISPs.

Nor did the actual words of the executives of some of the companies Singer mentioned, when they specifically said that reclassification would not impact their investments. On and on and on …

AT&T

AT&T is Exhibit A in Singer’s case. But for Singer to be right about Title II reclassification harming AT&T’s investment, AT&T would have needed the ability to see the future.

AT&T indicated as far back as November 2012 that its 2013–2014 capital spending would be higher than usual, “returning to normal levels in 2015.” See AT&T’s press release of Nov. 7, 2012.

This temporary bump was due to the company’s “Project VIP” upgrades to its business and residential broadband services, as well as its nationwide 4G-LTE upgrades. AT&T began telling investors early in 2014 that the project, initially expected to take three years, was ahead of schedule, and that it expected to see declines in capital spending sooner than originally thought.

And just as AT&T said it would, this decline started in mid-2014 — long before Title II reclassification was a realistic possibility in the FCC’s rulemaking proceeding around Net Neutrality.

In November 2014, AT&T put a firm estimate on its 2015 capital spending guidance, telling investors “[w]e expect 2014 to be our peak investment year for Project VIP and anticipate our Wireless and Wireline segments’ spend to be proportionally consistent to 2013. We expect our 2015 capital expenditures for our existing businesses to be in the $18,000 range.”

On Jan. 27, 2015, AT&T’s CEO reaffirmed this prior guidance, stating “capital expenditures will be in the $18 billion range, the same as we guided earlier, and that’s thanks to the completion of a lot of the Project VIP initiatives.”

On a July 23, 2015 call reporting the company’s second-quarter 2015 results, AT&T was asked directly by an analyst, “the $18 billion in CapEx this year implies a nice downtick in the U.S. spending. What’s driving that? Are you finding that you just don’t need to spend it or are you sort of pushing that out to next year?”

AT&T CFO John Stephens responded:

“Once again the network has done a great job in getting the Project VIP initiatives completed and when they’re done the additional spend isn’t necessary because the project’s been completed. And not for lack of anything but success. That’s what’s driving our changes. We continue to focus on working capital and construction work in progress and driving down cycle times and a whole host of other efforts the team is doing really good work on and that’s also helping out. But it’s really positive things that are driving this capability. We’re going to continue to invest in capacity. We’re going to continue to invest in successful sales.”

So, despite Singer’s bizarre exuberance in his claim that AT&T’s capital decline is “remarkable,” it’s not remarkable at all. The company told investors to expect it almost three years ago.

And when the decline started, AT&T told everyone why: We built stuff, it’s already built, we don’t need to build it again immediately, but we’re ready to invest more, and in fact, we have quite a few network upgrades we promised the FCC we’d make ahead of us.

Verizon

Verizon’s capital investments were down four percent for the first half of 2015 compared to the prior year.

But what Singer failed to mention is that Verizon’s capital spending on its wireless business was up by four percent. The overall drop was due primarily to continued declines in wired capital investments, which are due to the pre-planned winding down of FiOS builds, and which also long predate the FCC’s consideration of reclassification.

Nothing about the change in Verizon’s spending in the first half of 2015 suggests Title II (or anything else the FCC has done) is impacting the company’s investments. Wireless capital investment is up, as expected. Wireline is down, as expected.

There is nothing “remarkable” about any of this; it’s basic stuff that any serious industry analyst would know.

As Verizon CFO Fran Shammo said in January 2015, “I have been pretty consistent with this in the fact that we will spend more CapEx in the Wireless side and we will continue to curtail CapEx on the Wireline side. Some of that is because we are getting to the end of our committed build around FiOS; penetration is getting higher.”

It’s puzzling that Singer sees a nefarious regulatory causation behind Verizon’s small decline in capital spending, when he could have just listened to what Verizon itself said.

On the company’s first-quarter 2015 call, CFO Shammo said, “[a]lthough spending was slightly lower in the first quarter, we expect 2015 capital expenditures to be within our stated range of $17.5 billion to $18 billion.”

Shammo also repeated the company’s guidance on higher capital spending in 2015 than 2014 on its July 21, 2015 investor call.

Singer wants his audience to ignore the fact that Verizon’s CFO has repeatedly made statements like “our priorities are to invest in our networks through capital spending and spectrum acquisitions” (which Shammo said on April 21, 2015), and instead buy Singer’s baloney that FCC Chairman Tom Wheeler is hiding in the background and using Title II to depress investment.

CenturyLink

At this point, the story should be clear. But let’s trudge on.

CenturyLink is on Singer’s list, with a 9 percent decline, from $1.4 billion in the first half of 2014 to $1.27 billion in the first half of 2015.

Singer failed to note that CenturyLink’s fourth-quarter 2014 capital spending (which came during a period when it was increasingly clear that some form of reclassification would happen) was the highest ever for the company, and fails to realize (or pretends not to realize, more likely) that this higher spending at the end of 2014 may have impacted spending in the first half of this year (It did, according to CenturyLink’s CEO; read on).

But never mind all that. What was the company’s capex guidance for 2015, delivered to investors prior to FCC reclassification?

According to CenturyLink’s CFO, “approximately $3 billion,” or slightly lower than the $3.047 billion spent in 2014, which was slightly lower than the $3.048 billion spent in 2013, which was higher than the $2.9 billion spent in 2012.

To what did CenturyLink attribute the slightly lower capex after the fact?

On Aug. 5, 2015, CEO Glen Post told investors, “we have made significant investments in our network and data center infrastructure over the last several years and believe we have the flexibility to lower our planned capital budget by about $200 million to approximately $2.8 billion in full-year 2015, without significantly affecting our path to growth.”

So, capital spending is going to be down slightly from prior guidance, and according to the person in charge of CenturyLink it’s not because of any Title II-induced panic attacks that people like Hal Singer dream up but that never seem to trouble the ISPs themselves. It’s because the company’s past investments are paying off.

It’s also worth mentioning that on the same investor call, CenturyLink’s CFO noted that while capex would be slightly down in 2015, to $2.8 billion, the company would “expect full-year 2016 capital expenditures to be approximately $3 billion, inclusive of CAF-II requirements… ”

Which, translated, means the company’s capital spending will bump back up in the future because it committed to build broadband in rural areas in exchange for partial subsidies from the Universal Service Fund.

It’s bad enough that Singer focused on small fluctuations in quarterly spending, and ignored the company’s own explanation for this, but it’s even worse that he ignored CenturyLink’s broader commitment to expand and upgrade its network.

CenturyLink’s CEO just last month told investors:

“we continue to expand our gigabit footprint, ending the quarter with more than 600,000 households and 16 markets having access to gigabit speeds. We expect to have gigabit service available to approximately 700,000 households by year-end 2015, with plans for further expansion thereafter. We are also trialing technologies that enable up to 200 megabit over legacy copper networks. This is in the early stage, but it is showing good promise.”

So perhaps a lesson here: What a company builds probably matters more than how much they spent on building it, especially in an industry with declining costs.

Cablevision

Singer cited capital spending results from just two cable companies, Cablevision and Charter.

What he did not cite, however, is the fact that these cable companies helpfully report their capital spending broken down by money spent on the network itself versus money spent on things like set-top boxes. (And while he mentions Comcast’s spending on boxes only to discount it, even Singer wouldn’t be shameless enough to pretend that Title II impacts set-top-box investment.)

Cablevision’s total 2015 first-half capital spending was lower than it was in the first half of 2014, but this reflects lower spending on those set-top boxes and other cable TV-related expenses — not on Title II services and networks.

Indeed, Cablevision increased network investment in the first half of 2015 over the prior period. And Cablevision indicated that it expects second-half 2015 capital spending to increase, bringing the total for 2015 close to that for 2014.

Cablevision’s network investment (reported in the categories known as “Line Extensions,” and “Upgrades and Rebuilds”) was actually up 56 percent for the first half of 2015 compared to the first half of 2014.

The majority of the decline in Cablevision’s cable capital investments for the first half of this year is attributable to a decline in spending on the “Customer Premise Equipment” (CPE) category, accounting for $22.2 million of the company’s $39.2 million decline. This was fully expected based on Cablevision’s prior CPE spending and on the company’s continuing video-segment losses, in a segment that has nothing to do at all with Title II.

On its first-quarter 2015 earnings call, Cablevision CFO Brian Sweeney told investors that:

“[c]able capital spending in the first quarter was $134 million, a $12 million decrease from the same period in 2014. This primarily reflects lower CPE spending due to the timing of set-top box and modem purchases, partially offset by continued deployment of our smart routers and further investment in our network to support our new data offering and Wi-Fi expansion.”

Sweeney also noted that the first-quarter decline did not necessarily reflect the expected result for the rest of 2015:

“I would note that our first-quarter results were favorably impacted by the timing of several expense items, including marketing and employee-related costs, as well as the timing of capital spending. We continue to anticipate that 2015 total Company AOCF and CapEx, including incremental expenditures for Freewheel and our other new product initiatives, will be substantially similar to our 2014 results. However, as we have said before, this is a dynamic business, and we anticipate updating our guidance as the year progresses.”

On the Aug. 7 call discussing second-quarter 2015 results, Sweeney said:

“[c]able capital spending in the second quarter was $186 million, a $21 million decrease from the same period in 2014. This primarily reflects lower year-over-year spending on set-top box and modem purchases, as well as the timing of certain video-related projects. These declines were partially offset by higher project spending to support broadband and Wi-Fi expansion. We expect increased CapEx spending in the back half of 2015 as we continue to invest in the evolution of our product offerings and ensure a quality service experience.”

So, Cablevision’s decline in capital spending was mostly due to the fact that the company spent a large amount the prior year on set-top-box upgrades, and thus didn’t need to spend as much during the first half of this year on this expense that is wholly unrelated to Title II.

Furthermore, Cablevision’s actual network investments were up substantially, something Singer’s overly simplistic worldview suggests should not be happening.

Charter

Similar to AT&T’s, Charter’s 2014 capital spending was higher than usual, due in this case to Charter’s all-digital network conversion.

Charter completed this project at the end of 2014, as it indicated would be the case, and capital spending went down from the temporary high caused by that project.

However, as was the case with Cablevision, the bulk of the decline at Charter was due to lower spending on CPE (a segment that usually accounts for the majority of cable-company capital spending). Charter has largely completed its purchase of new set-top boxes and DOCSIS 3.0 modems needed for its upgraded all-digital services.

While Charter’s cable capital spending was down $326 million for the first half of 2015 compared to the same period in 2014, this was due to a $341 million reduction in spending on CPE, offset slightly by increases in other reported segments such as Line Extensions and “Support Capital.”

We know this is the case despite Singer’s irresponsible and misleading speculation. On the Charter fourth-quarter 2014 earnings call (which of course took place prior to the FCC’s February 2015 reclassification), CEO Tom Rutledge made it clear that capital spending would be down in 2015 because the company had completed its all-digital conversion:

“With all digital behind us, the capital intensity of our operations and our retained footprint will decline significantly in 2015, driving meaningful free cash-flow growth.”

Singer’s notion that this decline is somehow due to worries about Title II is just plain wrong. Singer is either ignorant of publicly available information and facts, or he’s willfully hiding those facts and misleading his audience.

Comcast

Curiously (or not so curiously based on the pattern seen above), Singer almost totally neglected to report on capital spending at Comcast, the nation’s largest ISP.

Maybe that’s because Comcast didn’t fit his tortured narrative. Even Comcast’s cable capex (i.e., capital spending excluding NBCU) is up 18 percent for the first half of 2015 compared to this period in 2014.

Thirty-seven percent of that increase is due to increases in spending on CPE (like the new X1 set-top boxes that Singer mentioned in passing), yet a full 22 percent of the increase stems from higher spending on what Comcast calls “Network Infrastructure” (or what it used to report separately in the categories of Scalable Infrastructure, Line Extensions, and Upgrades and Rebuilds).

Somehow this increase, and Comcast’s massive “Gigabit Pro” residential-fiber project, warranted nothing more than a dismissive mention in Singer’s misguided broadside against Title II.

Time Warner Cable

Time Warner Cable is nowhere to be found in Singer’s disastrously flawed research.

This may be due to the fact that, like Comcast’s, Time Warner Cable’s capital investments were substantially higher during the first half of 2015 than they were in 2014: up 16 percent. While nearly half (49 percent) of this increase was from CPE, 28 percent of it was in Line Extensions and Upgrades and Rebuilds, with another 16 percent of the total increase in Scalable Infrastructure.

What’s behind these increases? Time Warner Cable apparently realized that making modest upgrades to its systems increases its advantage over its slow DSL competitors, and those upgrades are especially needed in the few areas where it faces fiber competition (i.e., markets like New York City and Austin).

On July 30, Time Warner Cable CEO Rob Marcus told investors to:

“expect that full-year CapEx will be around $4.45 billion. Somewhat higher than our previous estimate, as we accelerate the TWC Maxx rollout and continue to upgrade and modernize our network and equipment. This is all part of our overall plan to drive meaningful operating and financial growth in 2016.”

So contra Singer, the nation’s third-largest residential ISP is increasing its network investment.

Using Comcast’s categorization of “Network Investment” (which includes core network spending on Line Extensions and Upgrades and Rebuilds, as well as support capital that includes things like headend equipment), network investment at the top four publicly traded cable ISPs was up 11 percent in the first half of 2015 compared to 2014.

These four companies account for nearly half of the entire broadband market, and nearly two-thirds of the market at the FCC’s 25 megabits-per-second definition.

Singer also overlooks ISPs like Google Fiber, Ting, Sonic.net, and others, all of which are investing in new competitive fiber-to-the-home services.

Capital investment is also up at T-Mobile (by 15 percent) and Sprint (by a whopping 61 percent). Initially omitting these two national wireless ISPs is quite curious, since they already operate with substantially lower margins than the dominant Twin Bells AT&T and Verizon.

If Singer’s theory of Title II investment harm had any validity whatsoever, these companies with little margin to spare would be the ones most expected to curtail spending. Yet even with Title II applied affirmatively to mobile-data services, these companies feel confident enough to expand investment.

In an update to Singer’s post, he did mention that if Sprint and T-Mobile were included, his overall estimate of the market’s decline would drop to 8 percent. He never explains fully which companies he uses to arrive at this new result.

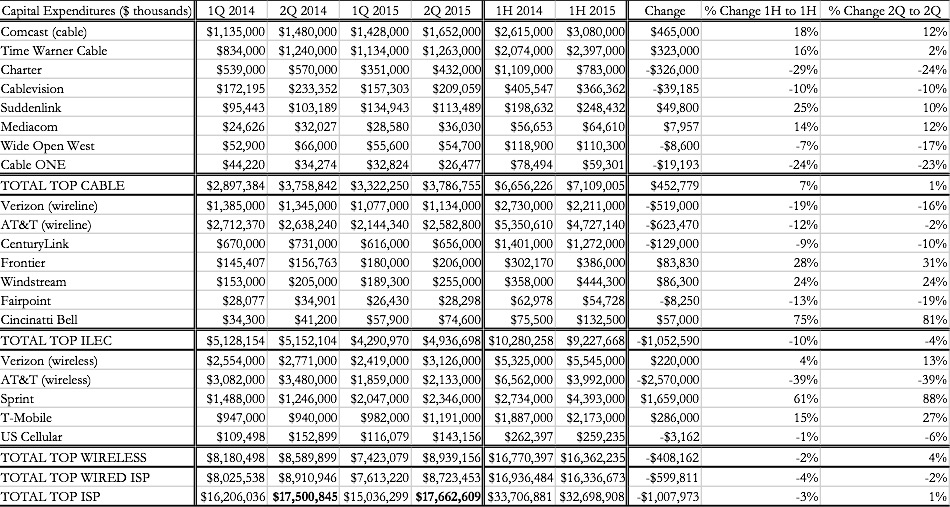

We looked at capital spending by all the top publicly traded wired and wireless ISPs (the cable companies discussed above plus Suddenlink, Mediacom, WOW!, and Cable ONE; the three local telephone companies discussed above plus Frontier, Windstream, Fairpoint and Cincinnati Bell; and the four national wireless carriers plus US Cellular).

The data (in the table below) shows an overall decline of capital spending from the first half of 2014 to the first half of 2015 of 3 percent ($33.7 billion in the first half of 2014, $32.7 billion in the first half of 2015) — most of which is fully explained by the analysis above on the declines in spending that AT&T, Verizon and others predicted long before the FCC reclassified.

Also notable from this data is the change in capital spending from second-quarter 2014 to second-quarter 2015.

If Singer’s theory had any validity, the results from the second quarter of 2015 should stand out, as it was the first full reporting period after the FCC’s vote. It turns out that capital investment was one percent higher after the FCC’s vote than it was for the same second quarter in 2014, the year prior to the vote.